The only article you need to read about your personal finances

✅ Investing ✅ Buying real estate ✅ Taxes and ✅ Savings. The only guide you need for your personal finances.

Providing for old age, but how? Is property or the stock market the better choice? The little 1×1 for taxes and how to survive a stock market crash.

The most pressing questions for your finances, explained in just one (slightly longer) article. Get your finances in order and in peace.

At a glance

- In most countries, the state pension will not be enough to maintain your standard of living. You are responsible for your own finances and pension, neither politics nor interest on your savings will do this for you.

- Financial Advisors are usually salespeople with the aim of concluding as many or as expensive contracts as possible — which are often not the best choice for your situation.

- Set yourself clear and measurable goals so that you can realize your dreams. How much money do you need by when, and what does that mean for your monthly savings rate by then?

- Start investing as early as possible. Even if it's a low savings rate at the start, the compound interest effect becomes stronger with every year.

- Health insurance, liability insurance and occupational disability insurance are a must, most others are not.

- Real estate is not always the best decision financially and can cost a lot of work, follow-up costs and flexibility. But if it's your dream, it's typically worth it.

- You can hardly avoid shares when it comes to retirement provision. If you diversify and use low-cost passive funds (such as ETFs), you can hardly go wrong. It's easier than you think!

- Use globally diversified ETFs and, depending on your risk appetite, fixed-term deposits as a security component to build up your assets.

Seven financial mistakes

The pension will somehow be enough

As things stand today, the statutory pension of most countries will only amount to a portion of today's income. Everyone, regardless of their income, must therefore expect that their pension will not be able to finance their current standard of living in the future.

John Smith, 45 years old, earns 35,000 dollar gross and retires in 2043 after 25 years in the job. His salary will increase by 2% each year, meaning that John will be able to receive a monthly pension of around 1,200 dollar at the age of 67. This is barely enough to cover rent, food and everyday expenses.

What is the pension level?

Ratio of average income to pension after 45 years of employment: the higher the pension level, the closer the average pension (known as the standard pension) is to the average income. The lower the level, the greater the pension gap. In other words, the difference between the previous salary and the pension payments increases.

Even in other calculation examples with significantly higher salaries, the inflation-adjusted pension is usually not even half of the salary. Accordingly, the pension level was only 48% in 2020.

The pension level is set to fall even further in the future. By 2030, the pension level is expected to fall to 45%. This is mainly due to demographic change.

Take away

No one can maintain their standard of living in old age with the state pension alone. Many would even be at risk of poverty in old age.

Money has made the world a worse place

Money as a means of facilitating exchange has advanced humanity. It forms the basis of the modern division of labor.

Without loans and investments, no major projects could have been financed, we would not have been able to build cities, health care and insurance would not have allowed the average age to rise.

If you are interested in how the world is changing for the better on the whole, I recommend the book Factfulness by Hans Rosling↗. Amidst the negative headlines, the positive developments in humanity are often overlooked. Hans Rosling shows in a vivid and understandable way why the world is better today than it was a few decades ago.

Take Away

When used correctly, money enables progress and finances better conditions for humanity. Without money, a modern society would not be possible.

You can only handle money well if you learned it early on

No. Much of what we need in life is not taught at school, university or by parents. This is also the case when it comes to finances.

Nevertheless, we learn new languages, how to start a family or how to raise dogs. So why shouldn't it be possible to learn about finance?

There are an incredible number of good blogs, websites, videos, podcasts, books, and people who teach financial knowledge. (Since you're reading an article about a book on finance, this is probably no secret to you 😜)

Key takeaway

At any age, it's possible to learn about finance.

Politics will take care of me

The state regulates many of the basics of our lives: peace in the country, basic infrastructure, free schools and universities and an independent judiciary. We don't have to worry about power cuts, so why worry about pension gaps?

On the one hand, because you have a responsibility to make the most of your money and on the other hand, it doesn't help you to mourn this hope. If you think that someone else (or the state) is responsible for your money, it prevents you from taking care of it.

Key takeaway

The desire for the state to take responsibility should not stop you from taking responsibility for your finances.

Low interest rates are to blame for my money not multiplying

You've probably already read a headline like "Interest rates fall to record lows". One conclusion is that wealth accumulation can't work. But that's not true.

Interest rate fluctuations and low interest rates have always existed. Savings accounts, endowment policies and call money accounts have not generated sufficient returns in the past either.

In particular, if you look at the real interest rate, interest rates have historically never been sufficient for retirement provision.

Nominal interest rate = the agreed interest rate, e.g. you get 2% interest on your account or pay 4% interest on a loan.

Real interest rate = nominal interest rate minus the loss in value due to inflation.

Example calculation: If inflation is 2.5% and you receive a nominal interest rate of 2%, then the real interest rate is -0.5% (2%-2.5%). In this case, your assets would lose 0.5% in value, even though you receive 2% interest from the bank.

Incidentally, low interest rates have led to an increase in value in other areas. Low interest rates often result in rising real estate prices and stock market prices.

Key takeaway

Important insight Interest rates alone are not enough to make retirement provision a success - and that has always been the case.

You can't do without a financial advisor

Some things sound complicated, and you're afraid of doing something wrong? That's why you need advice. Stop! There are two reasons not to:

- Advisors are usually actually salespeople. Depending on the structure, at least part of the consultant's salary depends on the contracts concluded. They therefore have a conflict of interest: providing honest advice or selling the most lucrative products possible. This is why the consultation itself is free of charge. They earn money from commissions or issue surcharges when the contract is concluded.

- Advisors only offer financial products from their own bank or insurance company. This means that they cannot offer you a more suitable product if it is from another provider. And other products are often better for you.

However, there are exceptions, namely fee-based advisors. You pay them a fixed fee, e.g. based on working hours. In return, they can advise you independently. However, the market share of fee-based advice is negligible.

Key takeaway

Advisors in the financial sector typically have a conflict of interest, and it is unlikely that they will sell you a product that suits your individual needs.

Set the course for your financial future

Those who formulate goals precisely and also plan what it will take to achieve them are less likely to be thrown off track. This is confirmed by motivational psychology.

People don't just wander around and realize they're standing on the summit of Mount Everest.

Zig Ziglar on the importance of goals

What does that mean for you? You should formulate your goal as specifically as possible. Instead of saying "I want to lose weight", it's better to say "I want to do 3 workouts a week" or "I want to lose 2 kilos in 10 weeks" and then break it down to "I want to lose 200 grams a week".

This is even more difficult with finances. How do you want to live? Do you want to retire early or finally become self-employed? Do you want to go abroad again? You may not be able to answer these questions precisely right now.

Even flexibility requires planning. If you want to keep the option of spending another 3 years abroad open, that's a goal. To realize this, you need a budget and at the same time you need to remain financially flexible. A real estate purchase that ties you down locally is then no longer necessary.

Key takeaway

Goals should be formulated in concrete terms, preferably with a number, and written down.

Turn dreams into goals

Take some time to write down your dreams and related goals. These questions will help you:

- What is my goal? To have 800 Dollar more per month in my retirement time

- When do I want to achieve this goal? At the age of 67, when I retire

- How much capital do I need for this? 800 Dollar net per month

- What do I need to do to achieve this goal? Save and invest X $ per month.

Is your goal realistic?

In other words, how big is the X from the 4th question? You can also approximate this:

- Calculate your target assets: In the example of the $800 private pension allowance, it could look like this. You estimate your life expectancy at 84 years, which results in a target amount of $163,200 (17 years of pension at $800 per month, 17 × 12 × 800 = $163,200)

- Determine your savings rate: How much of your income do you need to save each month until then (in the example, until you are 67 years old)? Let's assume you are 30 and therefore have 37 years to go. You would have to invest around $172 a month. Investing is the important part, because in this example an average return of 5% per year is priced in. A 5% return is also realistic, as you will see later.

- Is the $172 not in it right now? Maybe you can adjust your target. You can always adjust it upwards later - after a pay rise, for example.

You can't yet determine exactly how high your (state) pension will be at the end. Laws and taxes may change or food may become more expensive before you retire. Life expectancy is also difficult to estimate ... You won't be able to predict everything 100%. But with financial planning, you can remain flexible and keep making adjustments.

Key takeaway

The best way to deal with an uncertain future is to regularly review your goals and progress.

Start as early as possible

Because the magic trick is called the compound interest effect. The earlier you start investing, the longer the compound interest effect has time to help you.

Explanation Compound Interest Rate

Compound interest means that you not only receive interest on the money you deposit, but also on the interest you receive. So you receive interest on the money you deposit. And then, later on, interest on the interest you have already received. And the longer this goes on, the more interest you receive over time.

Example: Let's assume you invest 1,000 dollar at an interest rate of 5% per year. After one year, you will have 1,050 dollar. Everything is still normal here, and no compound interest is involved. In the second year, you will not only receive 5% on the original 1,000 dollar, but also on the 1,050 dollar. In other words, your deposited money and the 50 dollar interest earned in the first year. After two years, you are therefore entitled to 1,102.50 dollar. If you had only received the 5% interest on the money you paid in, you would have 1,100 dollar in the second year - i.e. 2.50 dollar less. That doesn't seem like much, but if you keep this up for a few years, this amount will increase year on year.

Two people invest $ 100 per month and receive an annual return of 5%. They retire at 65. The only difference is that Marie starts at 25 and Markus "only" at 35.

🙋♀️ Marie has almost $ 150,000 capital after 40 years of investing.

🙋♂ Markus has $ 80,000 capital after 30 years of investing.

🙋♀️ has just under $ 70,000 more than 🙋♂, although she has only paid in $ 12,000 ($ 100 per month for 10 years) more. The remaining difference of $ 58,000 is the return with compound interest.

Key takeaway

Start investing as early as possible - even if the amounts are still small - so that the compound interest effect can help you.

Your finances under the magnifying glass: where do you stand?

No goal without a starting line. That's why the first step is to find out where your assets stand.

Your net assets

This is everything you own, minus anything you still owe.

| Examples of assets | Examples of liabilities |

|---|---|

| Current account balance | Account overdrawn, credit card charged** |

| Overnight money, fixed-term deposit accounts | Loan (e.g. student loan)** |

| Savings book | Outstanding bills |

| Life insurance, pension insurance | Real estate loan** |

| company pension plan | car leasing |

| Home loan and savings contract | |

| securities, shares, bonds* | |

| Real estate, car, jewelry* |

*Assume the last or best possible estimated market value.

** Loan interest that you will have to pay in the future must be taken into account

Key takeaway

Important insight You can repeat an asset calculation regularly to keep an eye on the status quo.

Budget diary: an overview of income and expenditure

In companies, it's called cash flow; for you, it's simply a budget book. It helps you to keep track of what you earn and spend each month - and on what.

- Fixed costs: constant costs such as rent, cell phone bills, insurance, subscriptions, broadcasting fees, etc.

- Variable costs: weekly shopping, leisure expenses, shopping, new laptop, Pumpkin Spice Latte Grande To Go, etc.

You should keep the household diary for at least 3 months, preferably even longer, to get a realistic impression. You can also keep it retrospectively by going through your bank statements and writing them down.

The art of saving

Saving doesn't have to mean doing without. With a few tips, it can even be very rewarding. Your savings rate and savings ratio are important.

Saving can be fun

Savings rate and savings ratio

The savings rate is the amount of money you can put aside each month. But how much should it be? This is easier to calculate using the savings rate.

You calculate the savings rate by dividing the savings rate by your monthly net income.

We assume that you put aside $150 per month and that you receive $1,500 net per month as salary. Then your savings rate is $150 and the savings ratio is 10% (10% of your net income); a savings ratio of 30% would be better, i.e. $450 per month in this example.

A savings rate of 10% of your net income is the absolute minimum to build up a financial cushion.

Key take away:

Try to save at least 10 %, if not 30 %, of your net income.

Saving with the 3-account model

You don't need discipline to save, you need a system. A tried and tested system is the 3-account model.

- Salary and consumer account (current account): This is where you receive your salary, from which you pay rent, shopping and all your everyday expenses. Interest is not important for this account. From here, you set up a standing order to transfer your savings installment to the asset account every month (e.g. 2 days after receiving your salary).

- Rainy day account: Before you start investing, you should build up reserves for emergencies. The nest egg should be three to four months' salary. You can use an overnight money account here. A little interest is nice, but it's more important that you can access your money immediately in an emergency. You need to set up the account once and then not touch it again (or only in an emergency).

- Asset account (e.g. clearing account from the custody account): Once you have built up your rainy day fund, you can start investing. To do this, you transfer the savings amount from your salary and consumption account every month. This is a custody account for investing (more on this later).

Key take-away: The 3-account model with automatic standing orders is a system that lets you save without worrying about it.

Increase your savings rate with the savings booster

If you currently have a savings rate of 30%, for example, you may be able to increase this slightly the next time you get a pay rise. If the salary increase provides you with $100 more net income per month, you can use 50% of this, i.e. $50, for the savings rate. This means you will have more available each month, but you will still have increased your savings rate.

Let's assume that your salary increases by 2% each year and that you start saving 30% of your salary at the age of 25. If you save an additional 50% with every salary increase (i.e., half of the increase), your savings rate will have increased to 41% by your 65th birthday! That would be 18% more final assets.

A positive side effect is that you become less dependent on your income. If you didn't save because you were always spending your money on a more expensive standard of living, this would create a dependency. An expensive apartment, car or leisure activities create dependencies, which in turn require a large salary. However, wealth should actually create freedom instead of dependency.

Key take-away: You can use the savings bonus to increase your savings rate "on the side" and allow your standard of living to rise more slowly than your income.

Dealing with debt the right way

Don't worry, you're not alone if you're in debt. 77% of American houholds have at least some tpye of debt. Debt is not always an obstacle to your financial goal.

Good debts, bad debts

- "Good" debt means spending (other people's) money in the present so that you can benefit from it in the future. For example, a student loan, a promotional loan for further education, start-up loans and often a loan to buy a property.

- "Bad" debts are used in the present to live at the expense of the future. For example, a new car financed by a loan, a vacation financed by a loan, a television with zero-percent financing or a cell phone paid for in installments.

The money you have to pay back has no (great) value. You can't sell the car or cell phone financed by the loan for the same price. So it's already worth less than the loan you owe. Secondly, you usually have to pay interest on the loan. The overdraft interest on your account can quickly reach 7 to 16 percent.

If you were to repay a loan after 5 years with 16% interest, you would pay almost twice as much interest as the original loan was worth!

Good debt, on the other hand, creates value in the future. Studying enables a higher salary or the property can increase in value.

Key take-away: Consumer spending on cars, televisions or shopping makes you poorer and, in case of doubt, costs a lot of interest.

3 steps to freedom from debt

You should reduce bad debts as quickly as possible. You can do this in 3 steps:

- Analyze your debts: Sort your debts by total amount, interest (if any) and monthly repayment installments (if any)

- Optimize your debts: try to reduce the interest rates on one or more loans. With many banks, you can "restructure" loans, e.g. by changing the overdraft facility on the account to a loan agreement with lower interest rates.

- Use special payments: Try to reduce your debt further at every opportunity. Check whether you have special repayment rights that allow you to repay more in one go than in installments.

Longer repayments mean that you pay more interest on your debt. That's why it's generally a good idea to pay off your debts first and then invest. But it's also a good idea to start investing at the same time as paying off your debts to gain a sense of achievement.

Which insurance you need (and don't need)

Insurance minimizes the risk of financial loss but is also a (sometimes very large) cost factor.

Ask yourself each time whether the claim would cost you your (financial) existence. Or: Insurance is not worthwhile if you can pay for the damage out of your own pocket (from your nest egg).

Compulsory insurance

Important insurances

- Health insurance (if not given by employer or government)

- Only for those affected: motor vehicle liability, dog liability, builder's liability

- Private liability insurance: everyone should take out this, especially as it costs no more than two coffees a month. Liability insurance helps you if you accidentally or negligently injure someone (e.g. cause an accident) or break something. The damage can quickly run into millions.

- Occupational disability insurance: protects you against the loss of your ability to work (and consequently the loss of your income). The insurance pays out a fixed disability pension if you are no longer able to work or are only able to work less due to an accident or illness. This includes mental illnesses, such as burnout, as well as joint diseases. The costs of a "BU" depend heavily on your age, previous illnesses and occupation.

Insurance you may need

- Life insurance: In the event of your death, your relatives will receive a fixed sum insured. This makes sense if your family is financially dependent on your income.

- Building insurance: Protects landlords and owners against damage and disasters to the building.

- Foreign travel health insurance: You should also have health insurance abroad for the duration of your vacation. In North America in particular, an accident or illness on vacation can otherwise quickly turn into a financial debacle. It costs about one dollar per vacation day.

- Household contents insurance: Can be useful if you keep very valuable items in your home, as the insurance covers the damage in the event of fire, theft or natural disasters.

- Legal expenses insurance: It is difficult to estimate whether you will ever have to enforce your rights in court, for example to claim a job. You must take out the insurance at least 3 months before the legal dispute is foreseeable.

Insurance that you don't need

- Cell phone insurance

- Accident insurance (at most as an alternative if you do not receive a BU)

- Luggage insurance

- Glass breakage insurance

Changing and choosing insurances

You should check price comparisons from time to time to see if you can find better conditions. Insurance policies are often cheaper and you can save a few hundred dollar a year.

Key take-away: Cancel insurance policies that are not an existential risk.

The classics of investing money

Current account, savings book, call money: Non-profit investment

They combine the fact that you won't make any capital gains. However, they are very important as you can access your money at any time. You use the current account for your daily payments and the call money account for your emergency fund.

A fixed-term deposit account pays slightly more interest (than an overnight deposit account), but you have to leave the money there for a fixed period (usually between a few months and up to 10 years). It is therefore not suitable for a nest egg.

Life insurance, building society savings contracts

Home loan and savings contract

With a home loan and savings contract, you regularly pay a certain amount into the contract in order to receive a loan to build, buy or renovate a house in the future. As soon as enough money has been saved and the conditions are met, you can use the loan at a fixed interest rate - but you don't have to.

Nowadays, you hardly earn any interest during the savings phase. On the other hand, you could secure the current low interest rate on the loan for the next 10 years.

Financially, however, a home loan and savings contract is no longer really worthwhile. In most cases, you still have to pay costs and commissions, so the small state subsidy (less than $100 per year) makes no difference.

Do you have a home savings contract? If it's an old contract with a lot of interest in the savings phase, you can keep it. Otherwise, terminate it on time and use the money for better investments.

Private life and pension insurance

Life insurance is often used synonymously with the term pension insurance. In both cases, you pay monthly amounts that the insurance company manages and pays out in retirement (either regular monthly pension payments or as a lump sum). In the case of life insurance, dependents receive the money in the event of death.

Due to acquisition fees, commissions, costs and low returns, life insurance and pension insurance destroy your money.

Real estate - the rocky road to prosperity

Rent or buy? Or: why pay rent when the money could go towards real estate? Surprisingly, there are several reasons for this.

It is not enough to compare the monthly rent with the monthly installment with which the property loan is paid off

Example 1: Renting instead of buying

- 1,000 $ rent (cold) per month

- 20,000 $ saved

- can spend $1,300 a month on housing

Harry now has two options:

| Buy real estate | Renting |

|---|---|

| 1.300 $ financing the real estat | 1.000 $ for rent |

| no other investments | 300 $ investing (at an average of 5 % yearly profit) |

He has his eye on an apartment. This costs $250,000 plus $25,000 in incidental costs (estate agent, notary, etc.). Incidental purchase costs of 10% of the purchase price are normal.

The property is in good condition, so he expects maintenance costs of 1.5% per year. A loan that runs for 26 years would cost him 1.5% interest per year. His installment would therefore be $987.50 per month.

30 years later, Harry, who is renting, has total assets of around 332,000 $ and Harry, who is buying, only 303,000 $.

The increase in rent and the value of the property have been omitted for illustrative purposes.

Example 2: Buying instead of renting

In this scenario, all the parameters are the same for Harry, except for the basic rent. He pays $1,100 cold instead of $1,000 per month.

Now it would be worth buying. After 30 years, Harry would have built up $54,000 more wealth as a buyer.

Key take-away: Rent is not always wasted money. In purely mathematical terms, buying a property can be worthwhile instead - but by no means always

Factors when buying real estate

- Real estate as a burden: you lose flexibility when you buy. You have to pay off the loan every month and selling is not always easy. Particularly if the loan has not yet been repaid, it can cost several thousand dollar to cancel it with the bank.

- Changing requirements: the requirements for the property can also change quickly. Do you perhaps no longer like living in the country or do you need more space for the next generation?

- Maintenance cost trap: Older buildings can quickly incur maintenance costs of 2-3%.

- Refinancing: If you don't pay off the loan before it expires, you will have to take out a new loan for the remaining debt - possibly at higher interest rates.

- Lifestyle: In the end, a big part of the question is how you want to live your life. If a property is your big wish from an emotional point of view, you don't have to calculate the financial consequences down to the last detail. After all, it's your life choice - as long as the decision is well weighed up.

Rent out your property

You can use the rental income to finance the loan and build up further assets on the side. You can also deduct costs from your taxes. Sounds like a no-brainer. However, there are also disadvantages to renting out a property

- Bulk risk: you have one (or a few) properties. If something goes wrong there in the next 20 to 30 years, you won't have many other properties to make up for the loss.

- Letting is a second job: you get calls when the tap drips, have to juggle taxes and tradesmen, find new tenants and attend owners' meetings. The time involved should not be underestimated.

- Rental income is not guaranteed: Depending on which area the property is in, there may also be longer periods of vacancy.

- Low increase in value: From 1970 to 2020, residential properties in Germany increased in value by just 0.6 %. In some cities, of course, prices rose more sharply, but in other places prices have fallen. This is hard to predict.

- Costs incalculable: In addition to already unpredictable maintenance costs, you depend heavily on the behavior of the tenants. Do they ventilate well? Do they smoke a lot?

- Political change: In the next few decades, tax breaks may be overturned or new regulations may make being a landlord less attractive

- Competition with corporations: You are in competition with other landlords. And these are often groups with thousands of apartments. They can save on financing and maintenance costs and are therefore cheaper than you.

Key take-away A property is usually not the best decision from a financial point of view. Both for living in and renting out, buying a property has a lot to do with your desired lifestyle.

Other ways to invest in real estate

You can invest in real estate without buying (and managing) the properties yourself.

Real estate fund

With real estate funds, your money is managed together with that of other investors and invested in real estate. These investments are usually not recommended due to high fees.

Real estate investment via crowdfunding

Crowdfunding is processed via a platform that promises a fixed term and interest (usually 3 to 6 percent). The money is then used to implement the construction projects. This involves a major risk for investors, as their money is the last to be refunded in the event of insolvency.

Buying stocks of real estate companies

You can invest indirectly in real estate via shares in real estate companies such as Simon Property (USA). This is the most convenient way - more on this later.

Shares - how you can use the stock market to your advantage

The stock market is better than its reputation and an elementary component of financial provision. However, you shouldn't be unprepared.

What is a share?

A stock corporation is a company whose property is divided into many equal parts: the shares. When you buy a share, you become a co-owner of the company on a very small scale. With just a few dollar, you can become a shareholder and benefit from the company's success.

By owning a share, you can (usually) vote on decisions at general meetings and are entitled to receive dividends - if any are distributed. How many votes and dividends you have depends on the number of shares you own.

Earn money with shares

In addition to the dividend, you want to earn money primarily through a rising share price. If your share is worth $100 today and then rises to $150, you have made a price gain of $50.

You can easily buy and sell most shares on the stock exchange - quickly and easily. Like a marketplace, the stock exchange is a classified ad for shares. It is standardized (a share is always the same), regulated (supervisory authorities monitor companies) and efficient (a transaction can take place within seconds).

How is the price of a share determined?

Supply and demand. If many people want to buy a share, the price rises because there are just as many shares as before. People are willing to pay more to get one of the few available shares. The price rises. It can also fall if there is a lack of demand.

Price fluctuations are completely normal and have many reasons. Does someone currently have a large fortune and want to reinvest it? Does someone urgently need to liquidate their portfolio? All of this leads to fluctuations without anything changing in the company, and much is based on expectations.

A lot is based on expectations. If I believe that Tesla will present a great balance sheet next week, I buy shares now to benefit from the price jump. If many other people think the same, Tesla shares are already rising.

Fluctuations in value: Volatility explained

Volatility describes the fluctuations in the price of a share over time. Higher volatility typically means higher risk, as prices can change faster and in larger steps. Volatility is often measured by the deviation of returns from the mean over a given period.

Key take-away With a share, you acquire a small stake in the company and benefit from an increase in value and usually also from dividends. However, a lack of demand or poor expectations can also cause a share price to fall.

Risks on the stock market

Price fluctuations are the undisputed risk on the stock market. There are different types of risk.

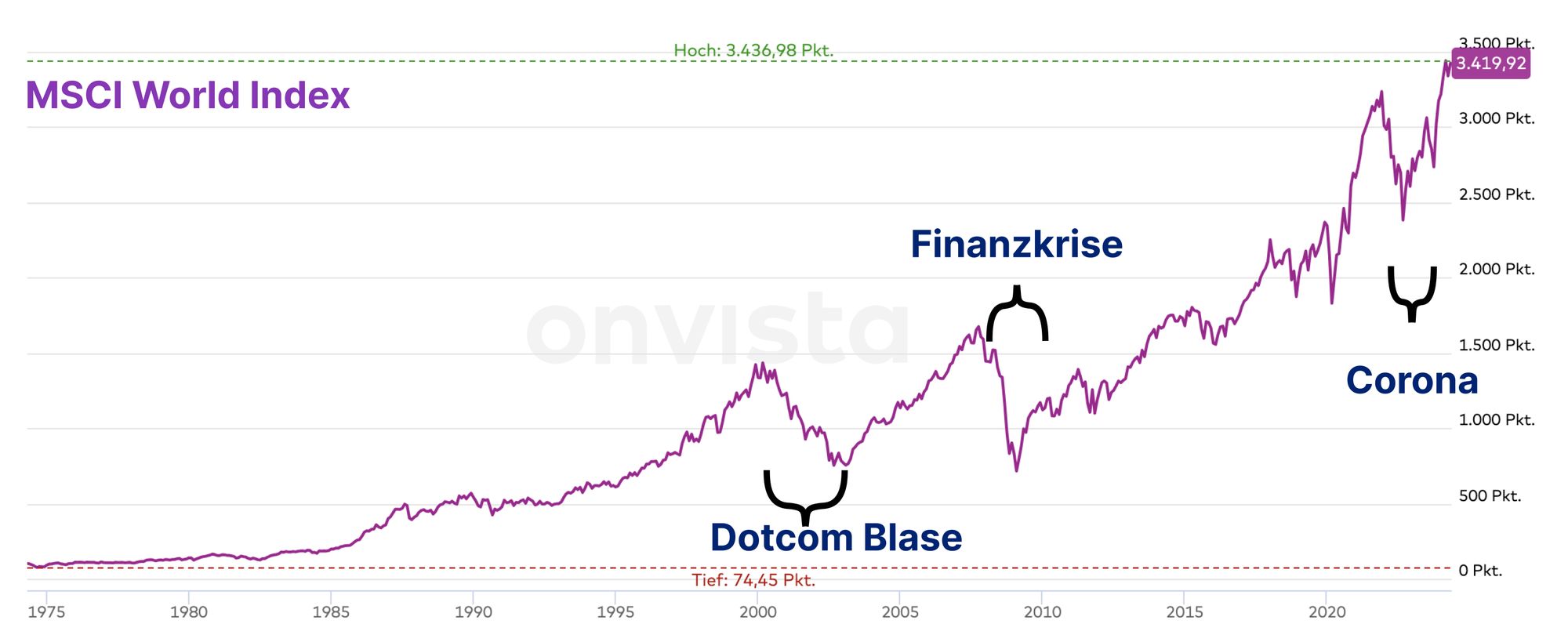

- Market risk: the risk that the majority of all shares lose value at the same time. This can be caused by changes in interest rates or events such as corona. As with corona, this can also mean a 30% loss. In the long term, however, all losses have always been recouped.

- Individual value risk/sector risk: Individual shares or sectors can also lose value, while the market as a whole does not lose value. This can happen, for example, if a specific company has delivery problems or legal regulations affect an entire sector.

Market risk is perfectly fine. It is unavoidable and unproblematic in the long term. Individual value risk, on the other hand, is bad risk. This risk is not rewarded (through higher average returns) and is easily avoidable.

Key take-away Individual stocks (or sectors) increase your risk unnecessarily. General market risk is unproblematic in the long term

Diversification as savior

"Diversification drastically reduces the risk of losing your investment. If you spread your money very widely, the individual value risk of a share becomes insignificant. But not - and this is the great thing - the return."

The average return is what makes shares so important for wealth accumulation: between 2002 and 2021, the average annual return on the global stock market was 7%.

Key take-away: Avoid unnecessary risk by diversifying into many stocks across many regions and sectors.

Investment funds and ETFs

The principle of a fund

Investment funds pool the money of hundreds or thousands of investors. This brings together a lot of money, which is then managed and invested by the fund company (or manager).

It is invested with the aim of increasing profits in

- shares (equity funds),

- real estate (real estate funds),

- bonds (bond funds)

- commodities (commodity funds)

- or a mixture (mixed funds)

invested. The criteria according to which investments are made can be found in the fund prospectus.

This is not a problem for you, because your money in the fund is special assets and is therefore not used to cover the fund company's debts. It is still your money.

Key take-away: You can diversify your money quickly, easily and securely using funds.

Index: the barometer for the stock market

An index defines a group of values (in this case shares) and measures how their value changes over time. There are around three million of these share indices worldwide (don't worry, only a few of them are relevant for you 😮💨).

You may be familiar with the S&P 500. It tracks the value of the most valuable companies in the USA. Another index, the MSCI World, tracks more than 1,600 companies from 23 industrialized countries.

Each index has its own criteria as to which companies are considered. In the S&P 500, one criterion is that the companies come from the USA. Other criteria are often the market capitalization, distribution of shares (e.g. no more than 70% of shares may be held by one investor) or environmental standards.

If, according to the rules, a company may no longer be represented in the index (e.g. in the USA, a company becomes more valuable than one that is included in the S&P 500), it is simply replaced.

You cannot invest directly in an index (an index is "only" the barometer, i.e. the benchmark). However, there are funds that replicate the indices and that you can buy.

Active funds vs. passive funds

In an active fund, there are people who observe and analyze the market and then buy and sell shares on behalf of the fund. Their aim is to generate as much return as possible. In return, however, these managers also receive fees from the fund, i.e. from you as an investor.

Passive funds track an index (e.g. the S&P 500 or MSCI World). The fund managers therefore copy the index without analyzing it themselves. As a result, the fees are much lower and the return is similar to that of the index.

| Active Fonds | Passive Fonds | |

|---|---|---|

| 🔎 Selection | Management actively looks for good investments | Replication of a market/index |

| 🎯 Goal | More return than the market | Exactly replicate the market return |

| 💰 Fees | High | Low |

Although they charge more fees, most active funds fail to generate more value than the index they are compared to. On the contrary, most managers generate lower returns in the long run.

Key take-away: Active funds cost more and usually generate less return.

ETFs: definition, advantages and disadvantages

ETF stands for Exchange Traded Fund. They are passive funds that replicate an index (e.g. S&P 500 or MSCI World).

ETFs have some advantages:

- ETFs are cheap: fees of between 0.1 and 0.8% per year are normal. And that makes a huge difference, as in the example with an investment of $50,000 over 20 years, with a return of 5%. There it makes a difference of over $30,000 or 1.45%.

- ETFs are (normally) diversified: If you use a global index across all sectors (e.g. MSCI World), you have maximum diversification.

- ETFs are emotionless: Unlike active funds, there is no one who buys or sells out of emotion, greed or panic

- ETFs are suitable for everyone: you can pay into an ETF using a savings plan starting from one dollar.

- ETFs are liquid: you can always buy or sell them when the stock exchange is open

Example comparing average ETFs and Fonds:

| ETF | Fund | |

|---|---|---|

| Management fee | 0.3% p.a. | 1.5% p.a. |

| Issue premium | - | 5.0% |

| Costs | -7,379 $ | -38,150 $ |

| Final amount after costs | 125,286 $ | 94,515 $ |

Risks of ETFs

- ETFs can tempt you to gamble: you could be tempted to buy and sell frequently because access is so easy

- Many ETFs are speculative: thematic ETFs, such as clean energy or blockchain, only represent a few companies based on a specific theme or region. These are not diversified and carry a significantly higher risk. You should therefore invest in broadly diversified ETFs.

- ETFs can also lose money: the market risk still exists. It is possible that stocks worldwide will fall in a few years - and with them your ETFs. But if you don't sell then, there is a very high probability that you will still generate returns over a long period of time.

Many providers allow you to save for ETFs automatically with a savings plan. Then, for example, your amount (e.g. $50) is debited from your current account on a monthly, weekly or annual basis and invested in the ETF.

Key take-away: ETFs offer you a very cheap way to invest in a diversified and long-term manner - much better than active funds.

Should you invest actively or passively?

Active investors select stocks specifically and must know the industry, analyze balance sheets and regularly buy and sell actively.

Passive investors invest (via an ETF) emotionlessly, consistently and for the long term. The approach is also called buy and hold.

The second group probably sounds more pleasant to you. The good thing: you will most likely do better with it! Statistically speaking, the second group makes more profit.

Why buy and hold usually brings more profit

There are two reasons for this

- Regression to the mean: Deviations from the average level off over the long term. If you hold a lot of stocks for a long time, your return is likely to be similar to the average return on the stock market. And that's where the next point comes in.

- The mean of stocks tends to rise: in other words, it's likely that the value will increase over the long term.

If you had held the MSCI World in any 15-year window between 1969 and 2018, you would have made at least 1.2% return per year. With a 40-year window, even at least 6%. So even the bad entry point (just before a stock market crash) and the bad exit point (during the stock market crash) would still have generated returns over a long period of time.

4 steps to your first investment

- Determine your balance between security and risk

- Use a global portfolio

- Find suitable ETFs for your global portfolio

- Open a securities account

Step 1: Determine the balance between security and risk

We all have different perceptions of risk. Some people look forward to a parachute jump, for others a suspension bridge is too much. The probability of an accident is the same for everyone - and yet everyone assesses the risk differently.

The same applies to money. There can be years when prices fall and your investments are worth up to 40% less. Will you still sleep well?

If you sell your ETFs out of panic about further falling prices, your investment will not work. That's why you should minimize the fluctuations to a level that you feel comfortable with.

Two building blocks for determining fluctuations

- Return building block: You want to increase your money with the return building block. That's why global, diversified ETFs are suitable. However, these can fluctuate in value in the short term.

- Security building block: To cushion the fluctuations from the return building block, you can use fixed-term deposit accounts in the security building block, for example. The return is less important here - but you don't have any fluctuations in value.

Government bonds for the security component?

However, bonds are not necessarily suitable for the security component, because the interest on fixed-term deposits is often higher than the potential return on the bonds.

What is a bond?

A bond is a type of security issued by companies or governments to raise capital. The issuer (e.g. the company or the state) promises to repay the capital borrowed at a set time and to pay interest during the term of the bond.

Bonds are usually traded on the stock exchange, which means that you can buy or sell them, similar to how you buy or sell stocks.

As is often the case, this is a very personal decision. If you stay calm and believe in the long-term strategy even when 60% is in the red, simply don't look at the portfolio. In this case you can also use 100% as a return building block.

Otherwise, you can start with half in the security building block, for example, and slowly get used to fluctuations in value. Over time, you might then increase the return building block.

Key take-away: Classify your risk and only invest the "risk component" in an ETF.

Step 2: Build your global portfolio

Now we look at how you build your return component. We remember that the criteria for your passive strategy are:

- a passive fund

- global diversification

- simplicity so that you don't have to constantly check or adjust

There is an incredible amount of choice and combination options. That's why one of these five ways should help you:

Five ways to build your global portfolio

- One index as an all-in-one solution: A portfolio consisting of an index cannot be surpassed in terms of simplicity. The MSCI World already contains a good spread across industrialized countries (such as Germany, the USA, France, Japan) and sectors. However, emerging countries (e.g. China, India, Mexico, Brazil, South Korea) are missing. But there are also indices for these that include stocks from these countries. Examples are the FTSE All World, with 4,000 companies from industrial and emerging countries, with 90% of the shares coming from industrial countries. An alternative is the MSCI ACWI (ACWI = All Countries World Index) with 2,900 global positions.

- The 70/30 mix: To determine the mix of industrial and emerging countries yourself, you can also combine two suitable indices. The MSCI World contains around 1,600 stocks from industrial countries. You can combine this with an MSCI EM, for example. Actually, all indices with EM for emerging markets represent emerging countries. Many then use the mix of 70% MSCI World and 30% MSCI EM.

- Include Europe with the 50/20/30 mix: The strategies mentioned so far include the USA much more, while European companies play a subordinate role. That's why you could also add 20% European stocks to the 50% MSCI World and 30% MSCI EM. The Stoxx Europe 600 with the 600 largest companies from Europe is suitable for this. The MSCI World also contains European stocks (to a lesser extent), which means that the European share in the 50/20/30 mix is even over 20.

- Dividend portfolio for passive income: If you want to keep receiving dividends, you can choose a portfolio for this. One example is the FTSE All World High Yield Dividend Index (high yield = high return). This shows 1,600 stocks from industrial and a few emerging countries that normally pay high dividends. Dividends can motivate you, but - be careful - they are less conducive to long-term capital gains.

- Stocks in combination with real estate and raw materials: In this model, you use 90% for one (or more) stock ETFs (e.g. those mentioned above) and add 10% from real estate and raw materials. The best way to represent real estate is through companies from the real estate sector. The FTSE NAREIT Developed Markets, which includes the 100 largest real estate companies in industrialized countries, is a good option. These are also included in the MSCI World or FTSE All World, so it is not absolutely necessary. You can represent raw materials such as precious metals, agricultural products, oil or gas using the Bloomberg Commodity Index, for example. These normally fluctuate more than stocks, but increase diversification somewhat. However, you should not spend more than 5% on them.

Why dividends do not bring more returns

There are basically two reasons for this:

- Dividends do not contribute to the growth in the value of the company. Otherwise, the company could have invested the money, which would increase the value of the share in the long term.

- You pay taxes on dividends (above a certain amount). You pay them immediately. This money cannot then generate any further returns in the next few years. You reduce the compound interest effect.

Important terms explained: MSCI, FTSE, High Yield, EM, IMI, Stoxx, Commodity

- MSCI = Morgan Stancley Capital International; US index provider

- FTSE = Financial Times Stock Exchange; US index provider

- Stoxx = Swiss index provider (now part of Deutsche Börse AG)

- EM = Emerging Markets

- IMI = Investable Markets Index; means that smaller companies are also included here.

- High Yield = high return; typically companies that normally pay above-average dividends.

- Commodity = standardized raw materials

If you allow yourself to be tempted to speculate with individual stocks or thematic ETFs, you should do so in a second portfolio. This way you separate rational ("boring") retirement planning and gambling. This avoids you selling the rational investments in favor of games.Positive side effect: You can easily compare the returns. And, like me, you can see that the returns from gambling are really worse.

Key take-away: You can build your entire wealth passively, easily and safely with a simple portfolio.

Step 3: Find suitable ETFs for your global portfolio

Remember: index and ETF is not the same. In the previous step, you thought about the composition of the portfolio. Perhaps you now want to use the FTSE All World, MSCI EM or Stoxx Europe 600.

Then we have to find the right ETF for the index. There are over 20 ETFs for the MSCI World alone. Which one is the right one?

ETF names explained

- Name of the ETF provider, here Xtrackers (a subsidiary of Deutsche Bank). iShares (from Black Rock), UBS, Vanguard, Amundi and Lyxor are also common.

- Index, here the MSCI Emerging Markets. The ETF tracks this index. We have talked about the MSCI World, MSCI Emerging Markets, FTSE All World, Stoxx Europe 600 and FTSE All World High Yield Dividend, among others.

- Special labels, here ESG. ESG stands for Environmental, Social and Governance) and indicate particular sustainability.

- Regulation, such as UCITS. UCITS stands for Undertackings for Collective Investments in Transferable Securities and means that the ETF meets the security standards set by the EU. These include, among other things, that a maximum of 20% of the ETF may be invested in a single security and that the money is held as special assets, i.e. is not lost if the provider goes bankrupt.

- Distribution interval or method, such as 1C here. This indicates that the distributions are directly reinvested – more on this later.

You won't always find the payout interval (1C) or special labels in the name. Don't let that unsettle you.

Criteria for your ETF selection

ETFs that track the same index are very similar. You can hardly go wrong. You can find the ETFs on portals such as FondsWeb.

Important criteria - you should then select the ETF

- Fund volume: As a guideline, you should note that the volume of the ETF is at least 100 million Dollar.

- Costs - TER (Total Expense Ratio): The total costs that the provider deducts from the volume each year for managing the ETF. They are therefore not debited separately from your account. The TER should be as low as possible. Normally between 0.1% and 0.5%.

Where can I find these criteria & factsheet

You can find the most important criteria on the portals or from the depository provider itself. There is also a fact sheet for each ETF. This is usually 3 pages, in which the most important companies and key figures for the ETF are listed.

Tracking Difference

A tracking difference is sometimes stated in the fact sheet. This indicates how far the ETF deviates from the index. This is related to the TER or tax effects.

Other (optional) criteria for selecting an ETF

- Distribution: Some companies in the ETF distribute dividends. ETFs can either pass these on to you (distributing ETFs or DIST, DIS) or reinvest them directly (accumulating ETFs or ACC, C). With distributing ETFs, you regularly get some money back, but with accumulating ETFs, the value is higher after a few years. Statistically, accumulating ETFs bring a little more return - but ultimately the decision is almost irrelevant.

- Replication method: In physical replication (also DR; direct replication), the ETF providers buy the shares (according to the index). In synthetic replication, there is also an intermediary bank that holds the shares for the provider. But that makes no difference to you.

Key take-away: To find the right ETF, you have to pay attention to the TER, fund volume and, if necessary, the distribution.

Step 4: Open the depot

The depot is like a digital safe for your ETF. You usually open a clearing account at the same time as the depot.

Difference of broker and depot

Brokers and depots are often used for the same thing. Strictly speaking, the broker is a service provider that places your orders on the stock exchange. The depot is just the safekeeping of your shares. However, most brokers also offer a depot.

Since the depot providers differ in detail, you can pay attention to the following:

- Is your ETF suitable for a savings plan? Check whether you can automatically invest in the ETF(s) you have chosen via a savings plan.

- Where is it cheap? First check the depot management fees. Some are free, otherwise 10 to 50 $ per year is normal. Then check the transaction costs, i.e. the costs incurred per purchase of an ETF. Many savings plans are offered free of charge. However, other providers charge transaction costs per execution or a percentage issue premium.

Spread as a cost factor

Just for the sake of completeness, I'll mention the spread. The spread is the difference between the bid and ask price of a security. This range is basically the margin with which brokers earn their money.

However, this has little relevance for ETFs and savings plans, as they are traded frequently and the spread should therefore not show any major differences.

Open a depot and set a savings plan

Now that you have found a depot provider, you can open the depot directly. In most cases, this can be done within 5 minutes from the couch.

Find your ID and off you go. RIGHT NOW!

You can open a savings plan directly in your depot. To do this, find the WKN of your ETF (or the ETF itself) and set the desired amount.

🎉 Congratulations! First of all, give yourself a big pat on the back.

Keep your portfolio in balance

Or also called “rebalancing”. The idea behind it is that you check at regular intervals (e.g. always around Christmas) whether everything is still in balance.

In most cases, one part of the depot has developed differently than another. For example, the MSCI World has risen sharply, but the MSCI EM has fallen slightly. Then the MSCI World now has a higher percentage share of the portfolio than you had planned in your strategy.

- Profit component vs. security component: It is highly likely that the profit component (e.g. MSCI World ETF) has become more valuable at some point than the security component (e.g. fixed-term deposit account). Then you would have to bring the shares back to the desired level.

- Composition: The shares (e.g. 70% MSCI World and 30% MSCI EM) may also have shifted.

What you always wanted to know

When is the right time to start?

In 99% of cases: now.

- Age: You are never too young to start (think of the compound interest effect). And as long as you have at least 15 years before you need the money again, you can almost certainly increase the value with stock ETFs.

- Good timing: Wouldn't it be better to wait until the next crash? You can't realistically estimate when the perfect time is. It's more likely that you'll miss the right moment by waiting.

If you want to start with a larger amount, you can also split it up into 6-12 months in the savings plan to minimize the risk of a bad entry point. Instead of investing $10,000 once, you could increase your savings plan by $1,000 for 10 months.

Statistically, it has been more successful in the past to invest the large amount all at once.

Stock market crash as the final boss?

No. Although you will most likely experience at least one crash, with a diversified portfolio you shouldn't have to worry. The global economy as a whole also recovers regularly. On the contrary:

- Stock market crash as an opportunity: in times of crash you can buy more shares for the same money (and do this automatically via the savings plan). If you still have some money left, it is worth investing more.

- Adjust the portfolio weighting and reduce the safety component so that it makes up the actual share again as planned.

- You are the risk - not the crash: The biggest risk is that you take your money out of the stock market out of fear - and then miss the subsequent upswing. Visualize the MSCI World and trust in your diversified portfolio. Not investing is riskier - and a certain loss of value of your money.

Investing green

With a globally diversified ETF, you also invest in arms companies, oil companies and those that have poor working conditions in the production chain. Can you avoid that?

The answer to this is to provide sustainable investing. That is why there are ESG criteria. ESG stands for:

- Environmental,

- Social and

- Governance.

Companies and financial products should be evaluated based on the criteria in the ESG categories in relation to their sustainability and responsibility efforts.

You can recognize these ETFs by the ESG or SRI (Socially Responsible Investing) in the name.

How are sustainable ETFs created?

There are specialized rating agencies that evaluate companies based on ESG criteria.

- ESG ETFs often include the best-rated companies in each industry. This is called best-in-class.

- Critical industries are excluded, such as: B. the FTSE ex Fossil Fuels (without fossil fuels) or MSCI ex Controversial Weapons (no controversial weapons). These are called negative criteria.

- Positive companies are selected. For example, in the MSCI Women Leadership with companies with many women in the management level. These are called positive criteria.

The idea behind ESG is that bad companies are not included in the portfolio and therefore lose value.

However, what happens to the voting rights that the shares have has a much greater influence. To put it very simply, the providers receive the voting rights for your ETFs. And this allows them to influence company management.

Black Rock, one of the largest ETF providers, with the iShares brand, votes 76% against sustainable decisions. BNP Paribas, Robeco and Amundi do better. Read more in the rating from the NGO ShareAction.

By choosing the ETF provider, you have a simple lever for sustainable finance.

Where your money is kept in your account, your emergency fund or your fixed-term deposit also makes a big difference. You can find out why sustainable banks are so important in this article.

Disadvantages of sustainable ETFs

- Less diversification, especially if some sectors are completely excluded

- Real sustainability is not necessarily a given. If you take the most sustainable oil company (best-of-class), is that sustainable?

Advantages of sustainable ETFs

- Better for the conscience. Even if it is not perfect, the growth of sustainable investments shows that the topic is constantly increasing. This in turn provides an incentive to improve the methods.

- Higher returns: There is scientific evidence that "sustainable" ETFs generate higher returns than their conventional counterparts.

This is how you find your green ETF

- First, find the basic index. For example, the MSCI World.

- Then look for a "sustainable" alternative to it. For example, by searching for MSCI World ESG or MSCI World SRI

- Then preferably choose an ETF from a provider that uses voting rights to encourage companies to be sustainable. These are, for example, ETFs from BNP Paribas, Robeco or Amundi.

Key take-away: ESG, SRI and co. are only superficially sustainable. But by choosing a more sustainable ETF provider you can simply bring more sustainability into your portfolio.

Money and happiness

Finally, a thought that may be floating around in your head. Money alone does not make you happy. After all, you are not living to have a savings plan.

That is correct. But money is the basis for your freedom. For the decisions to go on a trip, quit your job and pursue a job that you find meaningful. Or to pursue your hobby.

A financial cushion and your retirement provision are the basis for you not burying your dreams because of a lack of money. Money can give you freedom in making decisions.

I hope you liked the article and found it helpful. I would be particularly pleased if you considered sustainability in your finances. Banks and investments are a big lever. On kinu.earth you will find lots of tips on sustainable finances and green banks.

Good luck and keep your eyes open when it comes to retirement planning. Philip from kinu.earth

Sources and more information

Kommentare ()